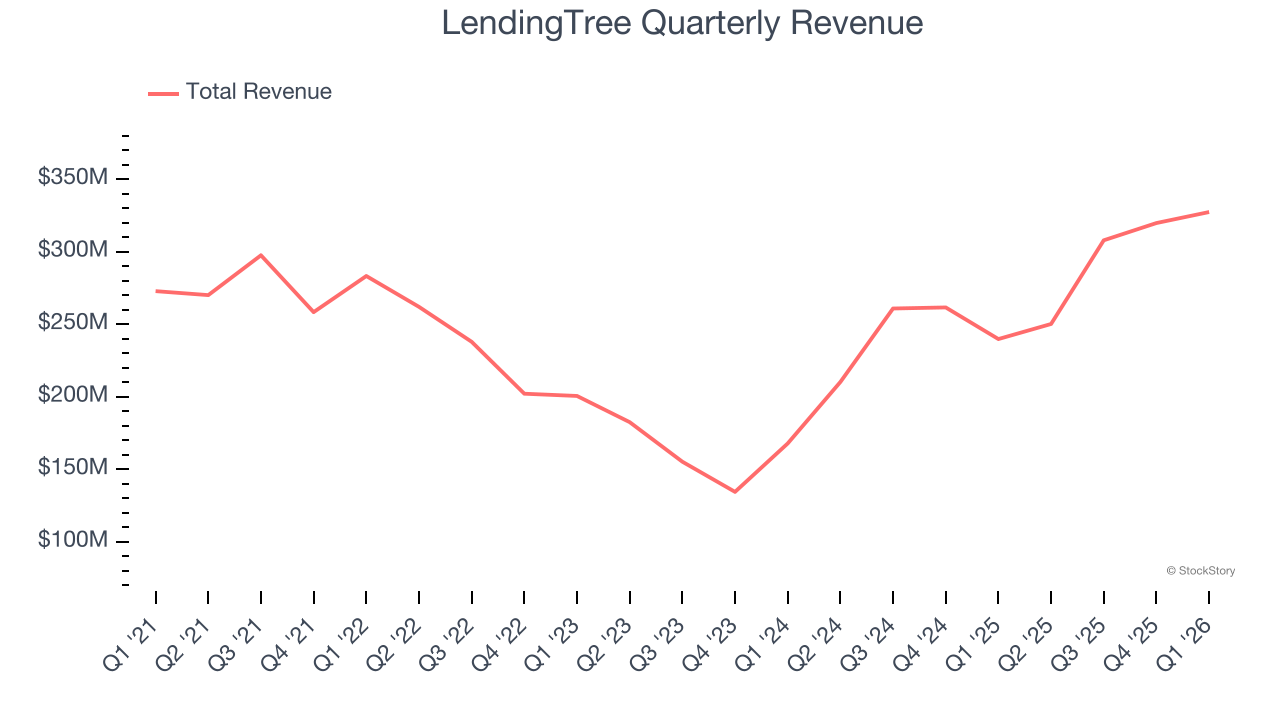

Financial marketplace platform LendingTree (NASDAQ:TREE) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 36.5% year on year to $327.3 million. Guidance for next quarter’s revenue was optimistic at $315 million at the midpoint, 2% above analysts’ estimates. Its GAAP profit of $1.22 per share was 34.2% above analysts’ consensus estimates.

Is now the time to buy LendingTree? Find out by accessing our full research report, it’s free.

LendingTree (TREE) Q1 CY2026 Highlights:

- Revenue: $327.3 million vs analyst estimates of $321.1 million (36.5% year-on-year growth, 1.9% beat)

- EPS (GAAP): $1.22 vs analyst estimates of $0.91 (34.2% beat)

- Adjusted EBITDA: $42.01 million vs analyst estimates of $40.05 million (12.8% margin, 4.9% beat)

- The company lifted its revenue guidance for the full year to $1.33 billion at the midpoint from $1.30 billion, a 1.7% increase

- EBITDA guidance for the full year is $157 million at the midpoint, above analyst estimates of $155.5 million

- Operating Margin: 9.5%, up from -3% in the same quarter last year

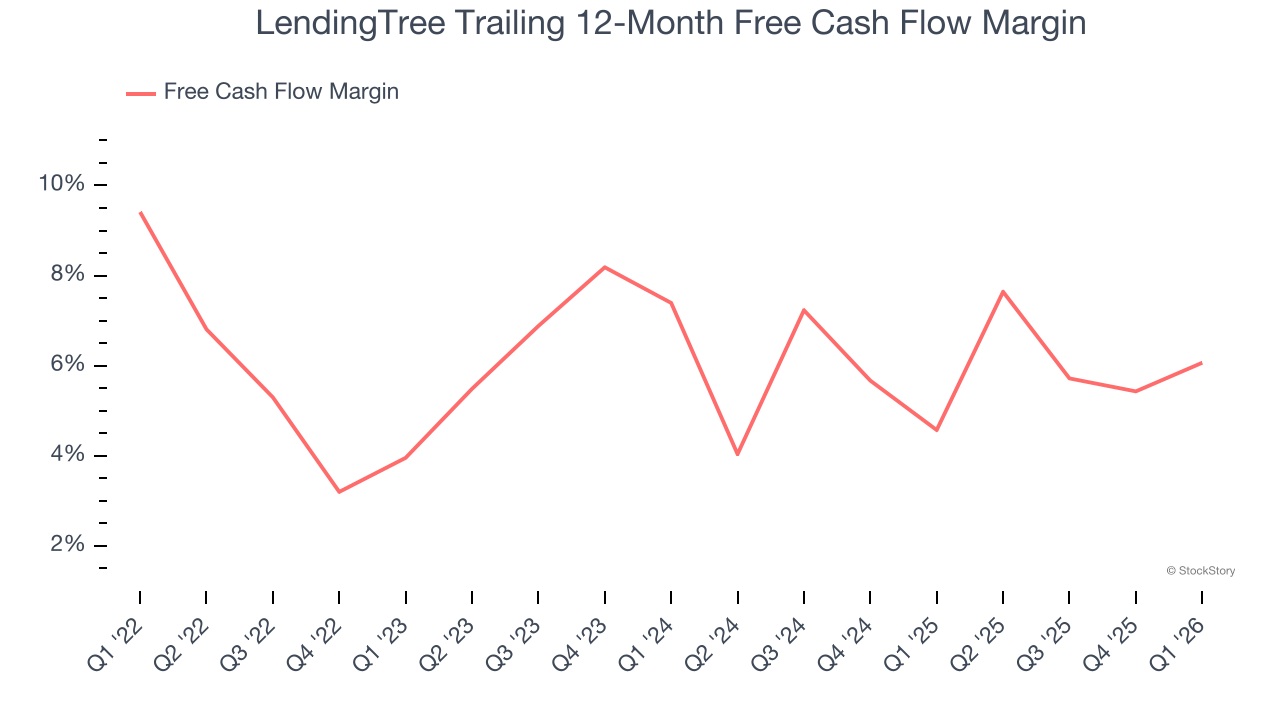

- Free Cash Flow Margin: 2.7%, down from 4.2% in the previous quarter

- Market Capitalization: $670.3 million

"We are thrilled to report first quarter AEBITDA grew 71% YoY. The Insurance segment produced another period of record revenue and segment profit, with segment margins posting a strong sequential increase as we optimize marketing spend. We operate the largest marketplace for consumers to shop for Insurance products. The industry broadly continues to benefit from healthy underwriting results, and our partners' appetite for new customers remains strong," said Scott Peyree, President and CEO.

Company Overview

Using the same comparison model that revolutionized travel booking, LendingTree (NASDAQ:TREE) operates an online platform that connects consumers with financial service providers across mortgages, personal loans, credit cards, insurance, and other financial products.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, LendingTree grew its sales at a decent 10.1% compounded annual growth rate. Its growth was slightly above the average consumer internet company and shows its offerings resonate with customers.

This quarter, LendingTree reported wonderful year-on-year revenue growth of 36.5%, and its $327.3 million of revenue exceeded Wall Street’s estimates by 1.9%. Company management is currently guiding for a 25.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.1% over the next 12 months, a slight deceleration versus the last three years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

LendingTree has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.4% over the last two years, slightly better than the broader consumer internet sector.

Taking a step back, we can see that LendingTree’s margin expanded by 2.1 percentage points over the last few years. This is encouraging because it gives the company more optionality.

LendingTree’s free cash flow clocked in at $8.78 million in Q1, equivalent to a 2.7% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

Key Takeaways from LendingTree’s Q1 Results

We were impressed by LendingTree’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also glad its EBITDA outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. Investors were likely hoping for more, and shares traded down 4.5% to $47.38 immediately following the results.

So do we think LendingTree is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).