Dover currently trades at $181.55 per share and has shown little upside over the past six months, posting a small loss of 5%.

Is now the time to buy Dover, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

We're swiping left on Dover for now. Here are three reasons why you should be careful with DOV and a stock we'd rather own.

Why Do We Think Dover Will Underperform?

A company that manufactured critical equipment for the United States military during World War II, Dover (NYSE:DOV) manufactures engineered components and specialized equipment for numerous industries.

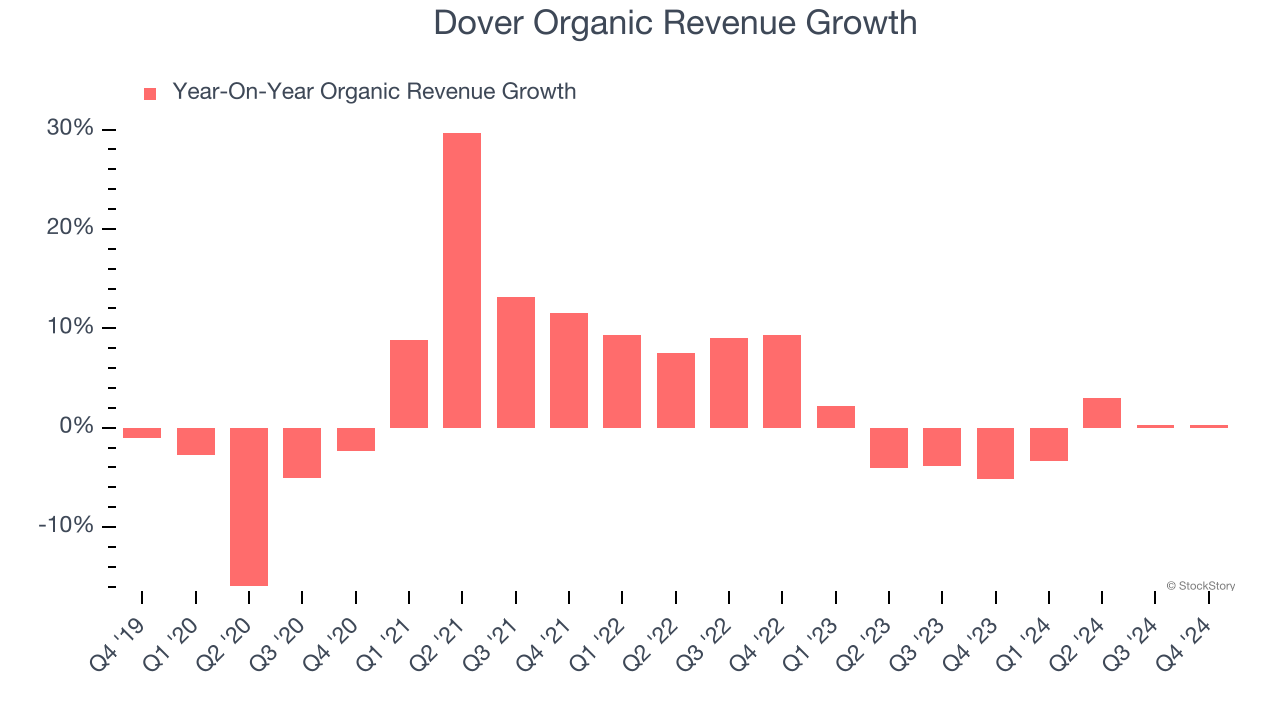

1. Core Business Falling Behind as Demand Declines

We can better understand General Industrial Machinery companies by analyzing their organic revenue. This metric gives visibility into Dover’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Dover’s organic revenue averaged 1.4% year-on-year declines. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Dover might have to lean into acquisitions to grow, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Dover’s revenue to rise by 3.4%. While this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

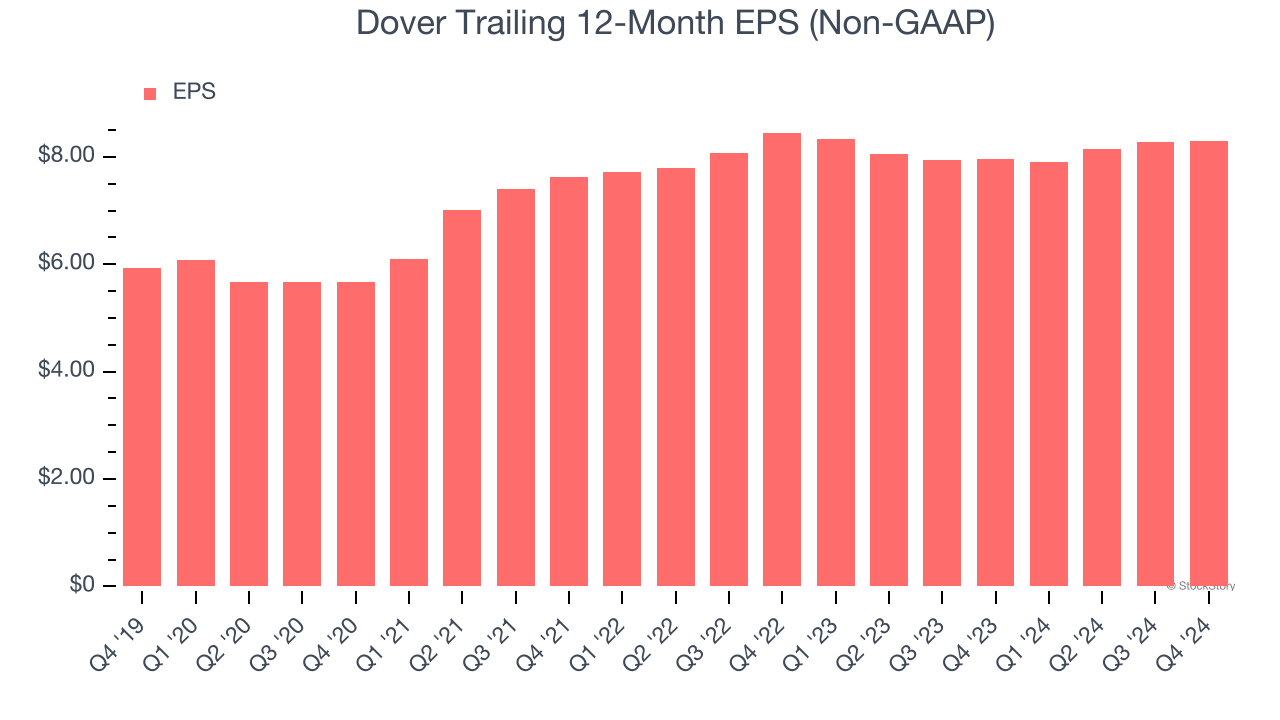

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Dover’s EPS grew at an unimpressive 6.9% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 1.7% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

Dover falls short of our quality standards. That said, the stock currently trades at 19.4× forward price-to-earnings (or $181.55 per share). This multiple tells us a lot of good news is priced in - we think there are better investment opportunities out there. Let us point you toward a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Dover

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.